Business owners look at their bank accounts and wonder. Is this good? Is this bad? Where did all the money go? That is where a profit and loss statement changes everything.

It simply shows whether a business finance made money or lost money over a specific period. It is one of the most important business financial statements any owner can understand.

When done right, a statement shows where money is leaking. It helps with tax planning. It guides business growth.

What Is a Profit and Loss Statement

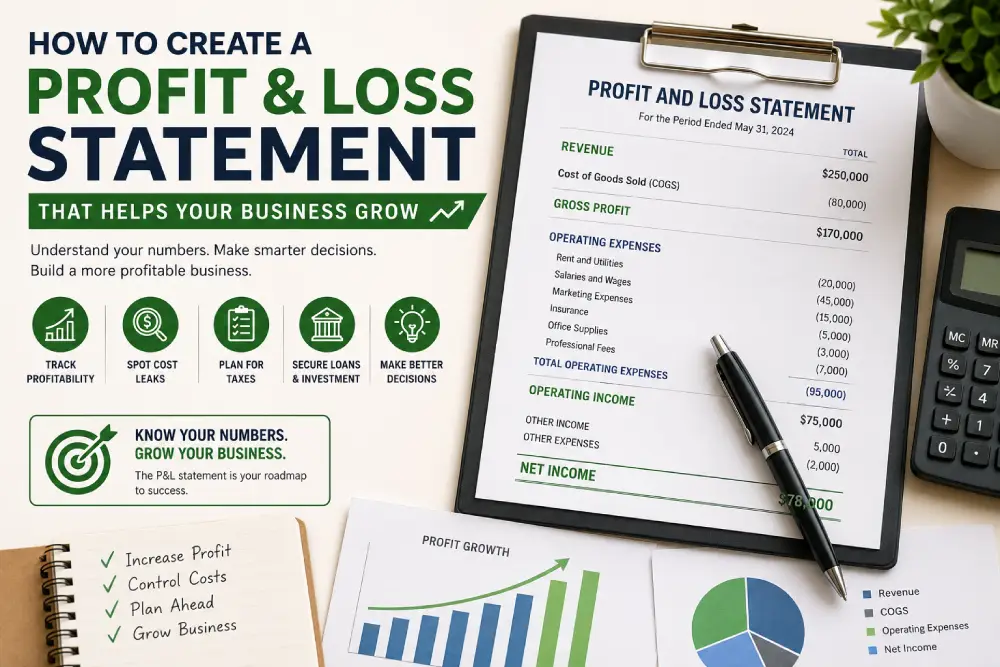

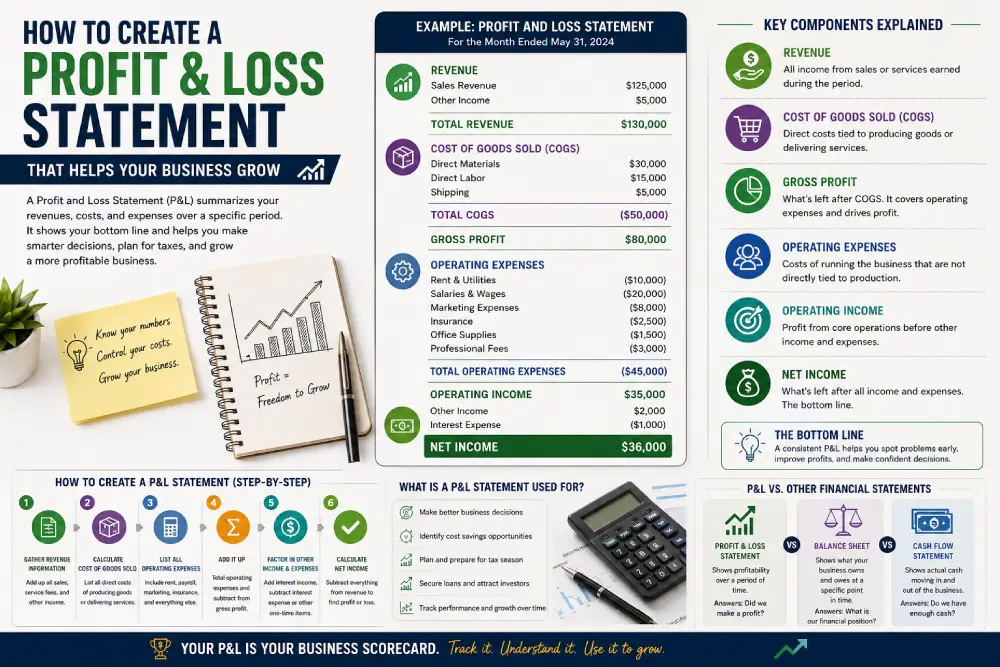

A statement is also called a P&L statement or income statement. It summarizes revenues, costs, and expenses during a specific period. Here is the simple formula:

Revenue – Expenses = Net Income

That is it. Everything else is just detail. It shows whether a business is making money or losing it. It is a financial report that shows how a business performed over time. Monthly, quarterly, or yearly.

Why a P&L Statement Matters for Business Growth

A P&L statement is not just for accountants. It is for owners who want to grow their business. Business success depends on understanding the numbers. Without a P&L statement, owners are flying blind. They do not know what is working. They do not know what is costing too much. They do not know if they are actually profitable.

A P&L statement helps with:

– Seeing which products or services make the most money

– Identifying unnecessary expenses

– Planning for tax season

– Getting loans or investment

– Making better business decisions

Financial health is measured by the P&L statement. It is the scorecard of the business.

Key Components of a Profit and Loss Statement

A P&L statement has several sections. Understanding each one is important.

Revenue

Revenue is all the money coming into the business. This is sales. It is services rendered. It is any income from core operations. Revenue should be recorded when earned. Not when paid. This is the accrual method.

Cost of Goods Sold

(COGS) is the direct cost of producing what the business sells. For a bakery, it is flour, sugar, and butter. For a service business, it is labor directly tied to delivering the service. It is subtracted from revenue. The result is gross profit.

Gross Profit

Gross profit is revenue minus cost of goods sold. It shows how much money is left to cover everything else. Rent, salaries, marketing, all get paid from gross profit.

Operating Expenses

Operating expenses are all the costs to run the business. These are not direct production costs. They are overhead. Common operating expenses include:

– Rent and utilities

– Salaries and wages (non-production)

– Marketing expenses

– Insurance

– Office supplies

– Professional fees

Net Income

Net income is what is left after all expenses are subtracted from revenue. This is the bottom line. This is profit. Positive net income means the business made money. Negative net income means it lost money.

How to Create a Profit and Loss Statement

Creating a statement is not difficult. It just requires organized numbers.

Step 1: Gather Revenue Information

Start with all income. Sales invoices. Service fees. Any money from core operations. Add it all up.

Step 2: Calculate Cost of Goods Sold

List all direct costs. Materials. Direct labor. Shipping. Anything tied directly to making the product or delivering the service. Subtract cost of goods sold from revenue. This gives gross profit.

Step 3: List All Operating Expenses

Go through every expense. Rent, utilities, marketing expenses, payroll, insurance, office supplies. Everything.

Step 4: Add It Up

Add all operating expenses. Subtract them from gross profit. This gives operating income.

Step 5: Factor in Other Income and Expenses

Any interest income or interest expense goes here. Any one-time gains or losses go here.

Step 6: Calculate Net Income

Subtract everything from revenue. What is left is net income. Profit or loss.

What Is a Profit and Loss Statement Used For

It is used for many things. It helps with tax planning. It shows business financial statements to banks. It helps owners make decisions.

Banks want to see a P&L statement before lending money. Investors want to see it before investing. Vendors may ask for it before extending credit.

Financial analysis starts with the P&L statement. It shows trends. It reveals problems. It guides strategy.

Profit and Loss Statement vs. Other Business Financial Statements

Business financial statements include three main reports. The P&L statement is one of them. Balance sheet shows what a business owns and owes at a specific point in time. Assets, liabilities, equity.

Cash flow statement shows actual cash moving in and out. Different from profit. P&L statements shows profitability over time. Revenue minus expenses equals net income.

All three are needed for a complete picture. But the P&L statement is where owners start.

How a P&L Statement Helps with Tax Planning

Tax planning requires knowing the numbers. A P&L statement shows taxable income. Tax planning becomes easier with an accurate P&L statement. Owners can estimate tax liability. They can make decisions to reduce taxes.

Spending decisions change when the numbers are known. Maybe buy equipment before year end. Maybe defer income. The P&L statement guides these choices.

Business Expenses and the P&L Statement

Business expenses are the heart of the P&L statement. Every expense must be tracked.

Some expenses are deductible. Others are not. Understanding business expenses helps with tax planning and financial analysis.

Business expenses include advertising, insurance, supplies, and salaries. Properly tracking them is essential for accurate statements.

How Often Should a P&L Statement Be Created

Monthly is the standard. Many businesses create a P&L statement every month. This allows for timely decisions. Quarterly and yearly statements are also important. They show long-term trends. The key is consistency. Create the P&L statement at the same time each period.

Conclusion

A profit and loss statement is not optional. It is essential for business success. It shows whether a business is making money. It reveals where money is going. It guides decisions.

Creating one is not difficult. Gather revenue. Calculate cost of goods sold. List operating expenses. Determine net income.

The P&L statement is the foundation of business financial statements. It helps with tax planning. It supports financial analysis. It drives business growth.

Every business owner should understand their P&L statement. It is the scorecard of the business.

Frequently Asked Questions

What is a profit and loss statement?

A profit and loss statement is a financial report that shows a business’s revenue, costs, and expenses over a specific period. It answers the basic question of whether the business made money or lost money.

What is the difference between a P&L statement and a balance sheet?

A P&L statement shows profitability over time. A balance sheet shows what a business owns and owes at a specific point in time. They are complementary business financial statements.

How often should I create a profit and loss statement?

Monthly is recommended. This allows for timely decisions and trend analysis. Yearly statements are also important for tax planning and long-term strategy.

What is the formula for a profit and loss statement?

Revenue minus expenses equals net income. This simple formula is the basis of the P&L statement. Everything else is detailed.

What are operating expenses on a P&L statement?

Operating expenses are the costs to run the business. Rent, salaries, marketing expenses, utilities, and insurance are common operating expenses.

Can I create a profit and loss statement myself?

Yes. Using accounting software or a spreadsheet, any business owner can create a P&L statement. Accuracy depends on good record keeping.

How does a P&L statement help with tax planning?

It shows taxable income. Owners can estimate tax liability and make spending decisions to reduce taxes. It is essential for financial planning.

What is cost of goods sold on a P&L statement?

Cost of goods sold is the direct cost of producing what the business sells. Materials, direct labor, and shipping are common examples.

Is net income the same as cash flow?

No. Net income is profit. Cash flow is actual cash moving in and out. A business can be profitable but still have cash flow problems.

Why is a profit and loss statement important for business growth?

It reveals patterns. It shows where money is leaking. It guides spending decisions. Without it, owners are guessing. With it, they make informed choices.